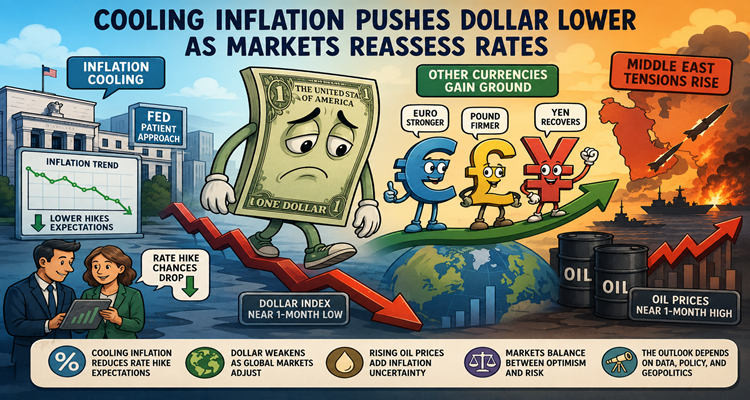

How Cooling Inflation Is Reshaping the Dollar and Global Markets

Key Takeaways

- Softer U.S. inflation data have weakened expectations of near-term Federal Reserve rate hikes, putting pressure on the dollar.

- Currency markets are adjusting rapidly as investors reassess interest-rate risks, growth prospects, and future monetary policy.

- Rising tensions in the Middle East are supporting oil prices, creating a potential new source of inflation uncertainty.

- Businesses, investors, and consumers worldwide could feel the effects through borrowing costs, trade flows, and commodity prices.

- The next phase for markets depends on whether inflation continues to cool or geopolitical shocks reignite price pressures.

Introduction

For much of the past two years, the U.S. dollar has benefited from one powerful advantage: higher interest rates. As the Federal Reserve aggressively tightened monetary policy to combat inflation, global investors flocked to dollar-denominated assets in search of stronger returns. That dynamic helped push the greenback to elevated levels against many major currencies.

Now, that narrative is beginning to shift.

Fresh signs of cooling inflation in the United States have prompted investors to rethink how much additional tightening the Federal Reserve may need. As expectations for further rate increases fade, the dollar has slipped toward its lowest levels in roughly a month, while rival currencies have gained ground.

Yet the story is far from straightforward. At the same moment, inflation appears to be easing, escalating tensions in the Middle East are lifting oil prices and threatening to create new inflationary pressures. The result is a market caught between optimism over cooling prices and concern about fresh economic risks.

Understanding this balancing act offers valuable insight into where currencies, interest rates, and global markets could head next.

Understanding the Development

Why the Dollar Has Lost Momentum

Currency values are heavily influenced by interest-rate expectations. When investors believe a country’s central bank will raise rates, its currency often strengthens because higher rates typically attract international capital.

Recent U.S. economic data have challenged assumptions that the Federal Reserve needs to act aggressively in the near term.

Measures of inflation have shown signs of moderation, while employment growth has also slowed compared with earlier expectations. Together, these indicators suggest that price pressures may be easing without requiring another immediate policy response from the central bank.

As a result, financial markets have sharply reduced expectations of a near-term interest-rate increase. That shift has reduced some of the support that previously helped the dollar outperform many of its peers.

How Other Currencies Are Responding

As confidence in further U.S. rate hikes declines, several major currencies have strengthened.

The euro has advanced as investors become more comfortable moving capital outside the United States. The British pound has also remained firm amid expectations of fiscal stability under Britain’s incoming political leadership.

Meanwhile, traditional safe-haven currencies such as the Japanese yen have recovered some ground after facing prolonged pressure from interest-rate differentials.

These movements reflect a broader rebalancing rather than a dramatic rejection of the dollar. Investors are simply recalculating relative opportunities across global markets.

Why This Matters

The Dollar’s Global Influence

The U.S. dollar remains the world’s dominant reserve currency. It plays a central role in international trade, commodity pricing, government reserves, and financial markets.

When the dollar weakens, the effects extend far beyond currency traders.

Many emerging economies benefit because their debt obligations become easier to manage when the dollar loses strength. Companies that rely on imported goods may also experience lower costs in local currency terms.

At the same time, American exporters can become more competitive because their products appear cheaper to foreign buyers.

Impact on Consumers and Businesses

Changes in currency values eventually affect everyday economic activity.

A weaker dollar can influence:

- Import prices

- International travel costs

- Commodity markets

- Corporate earnings

- Investment returns

For multinational corporations, exchange-rate movements can significantly affect profitability. Revenue earned overseas becomes more valuable when converted back into dollars, potentially improving earnings reports.

Consumers may notice impacts more gradually through product pricing, fuel costs, and broader inflation trends.

What Is Changing

Inflation Is No Longer the Only Story

Over the past two years, inflation has dominated economic discussions. Investors focused almost entirely on whether central banks would continue tightening policy.

Today, markets are entering a more nuanced phase.

The key question is no longer simply whether inflation is high. Instead, investors are asking:

- Is inflation sustainably declining?

- How resilient is economic growth?

- Will geopolitical events disrupt progress?

- Can central banks avoid overtightening?

This transition represents an important shift in market psychology.

Financial markets tend to move ahead of economic realities. Once investors become convinced that inflation is under control, they begin focusing on the next risks.

Oil Prices Have Re-entered the Conversation

One of those risks is energy.

Rising tensions involving the United States and Iran have pushed oil prices higher, raising concerns about future inflation pressures.

Energy costs affect nearly every sector of the economy. Transportation, manufacturing, agriculture, and consumer goods all depend on stable energy prices.

If oil continues climbing, businesses could face higher operating costs, potentially reversing some of the inflation progress seen in recent months.

This explains why investors remain cautious despite encouraging economic data.

The Bigger Picture

A Turning Point for Monetary Policy

Central banks around the world are approaching a critical moment.

For years, policymakers fought inflation through aggressive rate increases. Those actions slowed economic activity but also helped reduce price pressures.

Now, many economies are reaching a crossroads.

Continue tightening too aggressively, and policymakers risk slowing growth unnecessarily. Ease too soon, and inflation could return.

This delicate balancing act is shaping market behavior across continents.

The Return of Geopolitical Economics

Another notable trend is the growing influence of geopolitical events on financial markets.

For much of 2024 and early 2025, markets were primarily driven by economic indicators such as inflation reports, employment figures, and central bank statements.

Recent developments highlight how quickly geopolitical risks can reclaim attention.

Energy supply disruptions, regional conflicts, and trade tensions increasingly influence investor decisions. The interaction between economics and geopolitics is becoming more significant than many analysts anticipated earlier in the year.

For investors, understanding both dimensions is now essential.

Opportunities and Challenges

Potential Benefits of a Softer Dollar

A weaker dollar creates several opportunities:

Stronger Export Competitiveness

American goods become more attractive abroad, potentially supporting manufacturing and export-oriented industries.

Improved Emerging Market Conditions

Many developing economies borrow heavily in dollars. A softer dollar can ease repayment burdens and improve financial stability.

Better Global Liquidity

A less dominant dollar often encourages investment flows into international markets, supporting broader economic activity.

Risks That Remain

Despite these benefits, important challenges persist.

Energy-Driven Inflation

Higher oil prices could reverse recent inflation improvements and force policymakers to reconsider their strategies.

Policy Uncertainty

Markets may be underestimating how determined central banks remain to prevent inflation from reaccelerating.

Geopolitical Escalation

Further disruptions in energy-producing regions could create volatility across currencies, commodities, and equity markets.

The combination of these risks means investors should avoid assuming that the inflation battle has been permanently won.

What Comes Next

Three Scenarios Markets Are Watching

Scenario One: Inflation Continues to Cool

If upcoming economic data confirms that inflation is steadily declining, the Federal Reserve could maintain a patient stance.

This would likely keep downward pressure on the dollar while supporting equities and risk assets.

Scenario Two: Oil Reignites Inflation

Should energy prices continue rising sharply, inflation expectations could climb again.

In that environment, policymakers may be forced to maintain tighter monetary conditions longer than investors currently anticipate.

The dollar could regain strength as rate expectations increase.

Scenario Three: Economic Growth Slows Further

If economic activity weakens significantly, markets may shift attention from inflation toward recession risks.

This scenario could create mixed outcomes for currencies, as investors seek safety while also anticipating future rate cuts.

The Strategic Question Ahead

The central challenge for investors is determining whether recent inflation improvements represent a lasting trend or a temporary pause.

Market optimism currently favors the first interpretation. However, geopolitical uncertainty and volatile energy markets suggest caution remains warranted.

The coming months will reveal whether the global economy is entering a period of stable disinflation or preparing for another round of inflationary pressure.

Conclusion

The recent decline in the U.S. dollar reflects more than a reaction to a few economic reports. It signals a broader reassessment of how inflation, interest rates, and global risks are evolving.

Cooling price pressures have reduced expectations for immediate Federal Reserve action, weakening one of the dollar’s strongest supports. Yet rising oil prices and geopolitical tensions remind markets that inflation risks have not disappeared.

For businesses, investors, and policymakers, the challenge now lies in navigating two competing realities: an economy showing encouraging signs of stability and a geopolitical landscape capable of changing the outlook overnight.

The next chapter for the dollar and the global economy will likely be determined by which of those forces proves stronger.

The information presented in this article is based on publicly available sources, reports, and factual material available at the time of publication. While efforts are made to ensure accuracy, details may change as new information emerges. The content is provided for general informational purposes only, and readers are advised to verify facts independently where necessary.